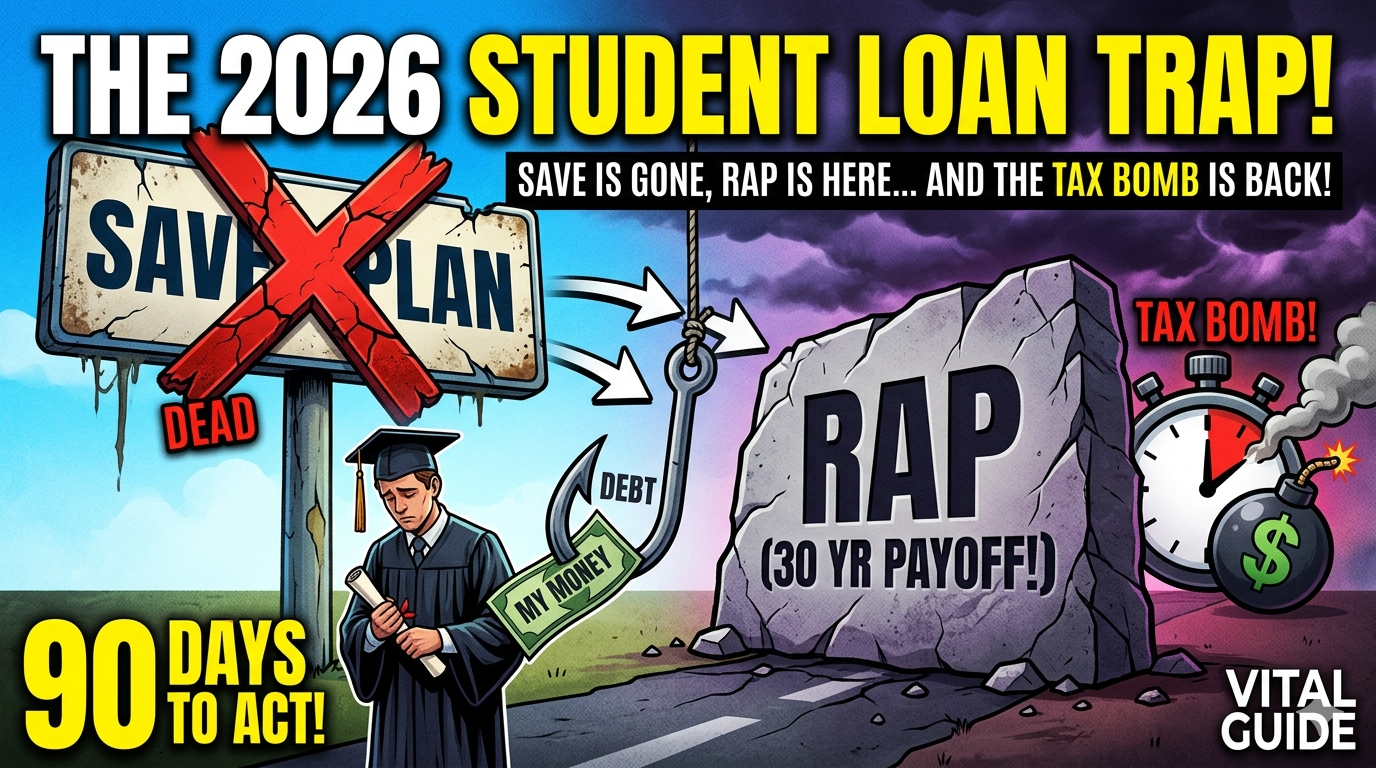

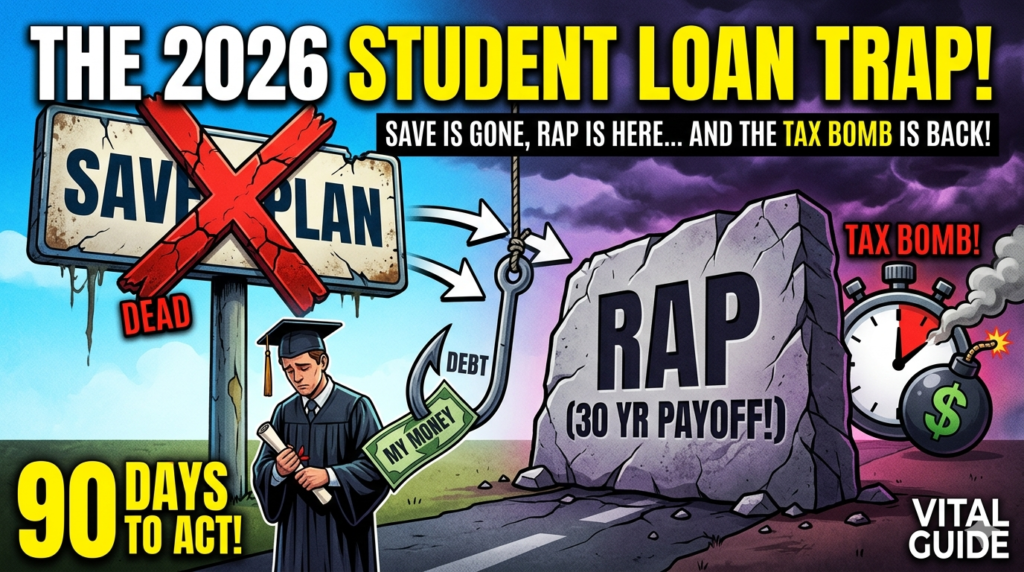

The 2026 Student Loan Revolution: How to Navigate the New Forgiveness Landscape and Save Thousands

The landscape of American student debt has just undergone its most radical transformation in a generation. With the official sunsetting of the SAVE plan and the rollout of the Repayment Assistance Plan (RAP) under the One Big Beautiful Bill Act (OBBBA), millions of borrowers are facing a “90-day transition window” that will define their financial health for decades. If you don’t act by July 1, 2026, you risk being defaulted into high-interest standard plans that could cost you your financial freedom.

Key Takeaways

- The RAP Era Begins: Starting July 1, 2026, the Repayment Assistance Plan (RAP) becomes the primary IDR option, capping payments between 1% and 10% of AGI but extending forgiveness timelines to 30 years.

- SAVE Plan Exit: Borrowers currently on the SAVE plan have exactly 90 days from July 1 to select a new plan or face automatic enrollment in costly Standard Repayment.

- PSLF Changes: New rules allow the Dept. of Education to disqualify employers based on “substantial illegal purpose,” requiring borrowers to re-verify employer eligibility immediately.

- Tax Liability Returns: As of January 1, 2026, discharged student loan debt is once again treated as taxable income at the federal level.

1. The Death of SAVE and the Birth of RAP: What Changed?

For the past few years, the Saving on a Valuable Education (SAVE) plan was the gold standard for low-income borrowers. However, following landmark court rulings in early 2026, the Department of Education has finalized a transition to the Repayment Assistance Plan (RAP).

The RAP is a double-edged sword. According to Bloomberg Finance, while it eliminates “negative amortization” (meaning your balance won’t grow if you make your minimum payments), it significantly pushes back the finish line. Unlike previous plans that offered forgiveness after 20 or 25 years, RAP generally requires 30 years of qualifying payments.

Understanding the Transition Window

If you are one of the 7 million borrowers previously enrolled in SAVE, your servicer will issue a notice on July 1, 2026. You have a 90-day grace period to choose between:

- RAP (Repayment Assistance Plan): Best for low-to-mid income earners seeking lower monthly out-of-pocket costs.

- IBR (Income-Based Repayment): Available for “old” borrowers (pre-2014) and some existing borrowers, offering forgiveness in 20-25 years.

- Standard Tiered Plan: A new fixed-payment option that scales over time as your income typically grows.

2. Public Service Loan Forgiveness (PSLF) in 2026: The “Illegal Purpose” Rule

The PSLF program remains a cornerstone for teachers, nurses, and government employees, but the 2026 update introduces a controversial vetting process. The Department of Education now holds the authority to disqualify specific non-profit employers if they are deemed to serve a “substantial illegal purpose” or run contrary to federal public policy.

What this means for you:

- Annual Recertification is Mandatory: Do not wait. Submit your Employment Certification Form (ECF) through the StudentAid.gov portal immediately to ensure your current employer still qualifies under the May 2026 guidelines.

- The 120-Payment Rule: The core requirement of 120 qualifying payments remains, but ensure your current repayment plan (likely moving to RAP) is considered “qualifying” under the new OBBBA regulations.

3. Data Summary: 2026 Federal Loan Repayment Comparison

To help you decide which path fits your “Vital” financial plan, we’ve summarized the core metrics of the new 2026 landscape.

| Feature | Repayment Assistance Plan (RAP) | Income-Based Repayment (IBR) | New Tiered Standard Plan |

| Monthly Payment | 1% – 10% of AGI | 10% – 15% of AGI | Fixed (increases every 2-3 yrs) |

| Forgiveness Term | 30 Years | 20 – 25 Years | None (Full Payoff) |

| Interest Subsidy | Prevents balance growth | Limited | None |

| Tax Impact | Taxable (Post-2025 rules) | Taxable | N/A |

| Best For… | Long-term budget stability | Those closer to 20-yr mark | High earners wanting out fast |

4. The “Tax Bomb” is Back: Preparing for the 2026 Reality

One of the most critical updates for 2026 is the expiration of the tax-free status for loan forgiveness. Under the American Rescue Plan Act, student loan discharge was federally tax-exempt. That exemption expired on December 31, 2025.

If you receive $50,000 in forgiveness in 2026, the IRS will treat that $50,000 as earned income. For a borrower in the 22% tax bracket, this could result in a $11,000 tax bill due the following April.

Vital Guide Tip: Start an “Insolvency Fund” or a dedicated high-yield savings account if you are within 5 years of forgiveness. Consult a tax professional to see if you qualify for “insolvency” status, which can sometimes mitigate this liability.

5. How to Apply: Your 2026 Action Plan

- Log in to StudentAid.gov: Ensure your contact information is updated. Servicers are currently overwhelmed, and missed emails could lead to automatic enrollment in the wrong plan.

- Consolidate by July 1: If you have FFEL or Perkins loans, you must consolidate into a Direct Consolidation Loan before the July 1st cutoff to maintain eligibility for the RAP or PSLF.

- Download Your Payment History: With the Education Department’s payment tracking tool currently offline, your loan servicer’s records are your only evidence. Download every statement now.

- Use the “Repayment Estimator 2.0”: The new 2026 tool on the FSA website accounts for the RAP vs. IBR variables.

Conclusion: Don’t Let the “90-Day Window” Close on You

The 2026 student loan changes are designed to simplify the system for the government, but they require aggressive proactivity from the borrower. Whether you are aiming for PSLF or navigating the transition from SAVE to RAP, the choices you make this month will dictate your net worth for the next three decades.

At Vital Guide, we believe financial health is as essential as physical health. Don’t let your debt metastasize through inaction.

[Take Action Now: Log in to your StudentAid.gov dashboard and verify your “Plan Transition Status” before the July 1st deadline!]

Sources:

- U.S. Department of Education: Final Rule on Repayment Assistance (May 2026)

- Bloomberg: The Economic Impact of the OBBBA on Graduate Debt

- Harvard Law: Analysis of the “Illegal Purpose” Clause in PSLF 2026

- Internal Revenue Service (IRS): Publication 970 (Tax Benefits for Education)